A Common Diaspora Question With a Straightforward Answer

Every year, thousands of Non-Resident Indians visit family in India and find themselves with the same logistical question: a tola of inherited gold from a grandmother, a wedding chain bought during an earlier visit, jewellery sitting in a bank locker for a decade – can it be sold in India for rupees, and can the proceeds eventually move back to a foreign account? The answer is yes on both counts, but the documentation, the bank account flow, and the repatriation limits are different from a resident sale. Get the steps right and the entire transaction can be done in a single day; miss one and the proceeds may sit in an Indian rupee account for months.

This guide is a step-by-step walkthrough for NRIs selling gold in India in 2026 – what documentation is needed, why an NRO (Non-Resident Ordinary) account is the natural settlement vehicle, how repatriation to NRE or directly to a foreign account works under FEMA rules, what tax applies, and what edge cases to plan for. Read it before your next India visit, and you will know exactly what to bring, where to walk in, and how the proceeds will flow back to you.

NRI Gold Sale at a Glance

| Eligibility | Any NRI / OCI / PIO holding gold acquired legally in India |

| Documents | Aadhaar (if held) + PAN + Passport + OCI/PIO card |

| Cash Limit | ₹1,99,999 per Section 269ST (banking channel above) |

| Settlement Account | NRO account preferred; resident SB account permitted |

| Repatriation Limit | USD 1 million per financial year from NRO |

| Tax Treatment | LTCG 12.5% above 24 months; STCG slab rate |

| TDS | Not applicable to the gold sale itself; TDS may apply to the remittance |

| Today’s 24K Reference Rate | ₹14,962 per gram (5 May 2026, IBJA) |

Today’s Rate (Same for Residents and NRIs)

The price you receive as an NRI is identical to what a resident receives – today’s live IBJA rate × tested purity, with deductions only for stones and solder at a reputable buyer. There is no separate “NRI rate” or “tourist rate”; the residency status of the seller does not affect the per-gram price. Use the live widget to confirm today’s 24K and 22K rates before walking into any branch.

Documents an NRI Needs to Sell Gold

NRI documentation is slightly heavier than a resident sale, primarily because of FEMA compliance and KYC requirements. Bring all of the following on the day of sale:

- Indian Passport – original. If you have surrendered it, bring the cancellation certificate plus your foreign passport.

- OCI card / PIO card – original (if you hold OCI status, this is mandatory; PIO cards have been merged with OCI since 2015).

- PAN card – mandatory for any sale above ₹2 lakh; useful for any transaction. NRIs can apply for PAN online if needed.

- Aadhaar – if previously issued; not all NRIs have it, but it speeds up KYC where available.

- Address proof in India – utility bill, bank statement, or any government-issued document with your Indian address.

- NRO account details – account number, IFSC, branch name (for IMPS/RTGS settlement).

- Foreign address proof – passport, foreign driver’s licence, or utility bill from the country of residence.

- Original purchase bills if available – optional but useful for source-of-funds documentation.

Why an NRO Account Is the Natural Settlement Channel

An NRO (Non-Resident Ordinary) account is a rupee-denominated savings account held by an NRI for India-side transactions. Income earned in India – including the proceeds of a gold sale – flows naturally into an NRO account, where it is taxed under Indian rules and from where it can be repatriated within FEMA limits. An NRE (Non-Resident External) account is also rupee-denominated but is meant for foreign-source income converted to rupees, with full repatriability. Gold sale proceeds cannot go directly into an NRE account because the income source is Indian; they must first land in NRO, where they sit until repatriated.

If you do not yet have an NRO account, almost every Indian bank – SBI, HDFC, ICICI, Axis, Kotak – offers them with online application and Aadhaar/passport-based KYC. Setup typically takes 7–10 working days. Plan ahead of your visit, or open the account during the visit and time the gold sale for after the account is active.

The Sale Process Step by Step for NRIs

- Confirm your NRO account is open and active before walking into the buyer. If not, open one first.

- Carry original Passport, OCI card, PAN, Aadhaar (if any), Indian address proof, and the gold to be sold.

- Walk into a branch of the buyer (Attica Gold has branches across Karnataka, Tamil Nadu, Andhra Pradesh, Telangana and Pondicherry).

- Watch the XRF purity test in your presence. Each piece takes 15–30 seconds.

- Receive the written line-by-line quote with weight, purity, applied rate, deductions and net amount.

- Complete enhanced KYC: Passport scan, OCI scan, PAN scan, Indian and foreign address declaration. Sign the FEMA-compliance declaration form.

- Choose payment mode: cash up to ₹1,99,999, IMPS to NRO above that. RTGS is available for amounts above ₹5 lakh.

- Confirm the bank SMS arrives in your NRO account, then leave with the signed invoice.

💰 Get the Best Price for Your Gold Today

Instant valuation • Transparent pricing • 100% secure & trusted

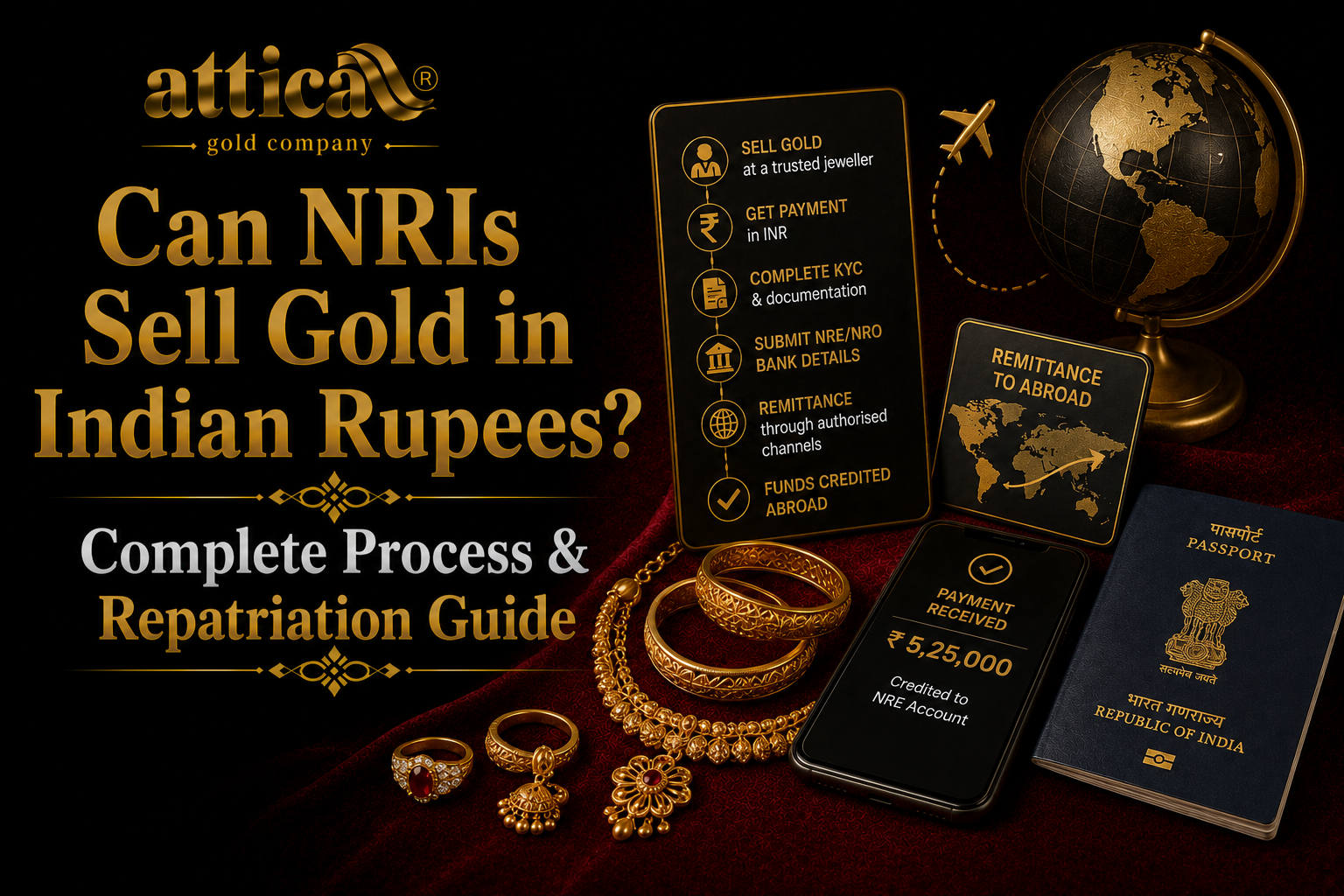

Repatriation: Moving Rupees to Your Foreign Account

Once the sale proceeds are credited to your NRO account, you have two repatriation paths under FEMA rules:

- Direct repatriation to your foreign bank account – up to USD 1 million (or equivalent) per financial year (April–March), subject to a Form 15CA + Form 15CB submission.

- Transfer to your NRE account – also subject to the USD 1 million limit per financial year, with the advantage that funds in NRE are then fully repatriable without further limits.

Form 15CA is a self-declaration filed online at the Income Tax e-filing portal. Form 15CB is a Chartered Accountant certificate confirming the source and tax compliance required for transactions above ₹5 lakh in a financial year. Most banks process the repatriation within 5–7 working days once both forms are submitted. The USD 1 million per financial year limit covers NRI gold repatriation along with all other NRO-to-foreign transfers, so plan large sales accordingly across financial years if needed.

Tax Treatment for NRI Gold Sales

NRIs face the same gold sale tax framework as residents, with one administrative wrinkle. Gold held over 24 months attracts long-term capital gains at 12.5% on profit (post-July 2024 budget, no indexation). Gold held under 24 months is short-term, added to the NRI’s slab income from Indian sources. The tax is calculated against the cost of acquisition (original purchase price, or fair market value on the date of inheritance for inherited gold).

TDS does not apply to the gold sale itself (sale of personal effects is outside the TDS scope), but the buyer reports the transaction in their GST returns linked to your PAN. When you repatriate, the bank may apply TDS on the transferable income unless you produce documentation showing the LTCG has already been declared and the tax paid via advance tax or self-assessment. The NRI gold tax rules are best handled by a CA familiar with FEMA – most large banks in India have empanelled CAs who issue Form 15CB for routine NRI repatriation.

Common Edge Cases NRIs Should Plan For

- Inherited gold without bills – fully sellable; XRF testing handles purity. Source of funds for repatriation requires a Will copy or a family settlement deed.

- Gold purchased on an earlier India visit when you were resident – provide original purchase bill if available; otherwise XRF + statement of acquisition is acceptable.

- Gold gifted by family – gift deed strongly recommended; otherwise, a written declaration with witness signatures.

- Sale value above ₹50 lakh in one financial year – triggers reporting under SFT (Statement of Financial Transactions) by the buyer; nothing to action by the seller, but expect downstream IT department visibility.

- Repatriation above USD 1 million in a financial year – not permitted under standard rules; requires special RBI approval. Plan multi-year repatriation if the total sale exceeds this.

- NRI account in foreign bank flagged for additional KYC – provide Form 15CA/15CB plus Indian source documentation; usually clears within 1–2 weeks.

Why Choose Attica Gold for NRI Gold Sales

NRI gold sales succeed or fail on the buyer’s ability to handle FEMA-compliant KYC, generate proper documentation for repatriation, and settle into NRO accounts cleanly. A buyer accustomed only to resident transactions may struggle with OCI / PIO documentation, foreign address declarations, or the Form 15CB chain. The right buyer has handled hundreds of NRI sales and treats them as routine – same XRF testing, same live IBJA rate, just with enhanced documentation.

Attica Gold runs the same protocol at every one of its 200+ branches across Karnataka, Tamil Nadu, Andhra Pradesh, Telangana and Pondicherry – calibrated XRF in your presence, today’s live IBJA rate displayed openly, written line-by-line invoice, NRI-specific KYC at the counter (Passport, OCI, PAN, FEMA declaration), and IMPS/RTGS settlement directly to your NRO account. ISO 9001:2015 certification means the same standard at every branch, every day. If you have been planning to sell inherited gold during your next visit to India, your wait is over. Bring your documents, take the test, and the proceeds will be in your NRO account before you leave the branch – ready for repatriation under standard FEMA limits.

Frequently Asked Questions

Can NRIs sell gold in India in Indian rupees?

Yes. Any NRI, OCI cardholder, or PIO can sell gold acquired legally in India, with proceeds settled in Indian rupees to an NRO (Non-Resident Ordinary) account. The price received is identical to what a resident would receive – today’s live IBJA rate × tested purity, with the same XRF testing protocol. The only differences are enhanced KYC (Passport, OCI card, PAN, foreign address proof) and the settlement account being NRO rather than a regular savings account.

What documents does an NRI need to sell gold in India?

Indian Passport (original), OCI or PIO card (original), PAN card, Aadhaar (if held), Indian address proof, foreign address proof, and NRO account details (number + IFSC). For inherited gold, a Will or family settlement deed is helpful for repatriation. For sales above ₹2 lakh, PAN is mandatory under Rule 114B. For sales above ₹5 lakh, repatriation requires Form 15CB from a CA in addition to the standard Form 15CA self-declaration.

How does NRI gold repatriation work after the sale?

After sale proceeds are credited to your NRO account, you can repatriate up to USD 1 million per financial year (April–March) under FEMA rules. The path is: NRO → NRE (rupee-to-rupee, but NRE is freely repatriable) or NRO → foreign account directly. Both require Form 15CA online filing; transactions above ₹5 lakh additionally require Form 15CB CA certificate. Banks typically process the transfer in 5–7 working days once forms are submitted. The USD 1 million limit applies to combined NRI gold repatriation and all other NRO-to-foreign transfers.

What are the NRI gold tax rules in India?

NRIs face the same capital gains framework as residents. Gold held over 24 months: long-term capital gains at 12.5% on profit (no indexation, post-July 2024 budget). Gold held under 24 months: short-term gains added to slab income from Indian sources. Cost of acquisition is the original purchase price, or fair market value on the date of inheritance for inherited gold. TDS does not apply to the gold sale itself, but tax must be paid via advance tax or self-assessment before repatriation.

Do I need an NRO account to sell gold as an NRI?

Not strictly required for the sale itself – small cash sales below ₹1,99,999 can be paid in cash directly. But for any sale above ₹2 lakh (which is most family gold), settlement must move through banking channels, and the natural channel for NRI Indian-source income is an NRO account. If you do not yet have one, almost every Indian bank offers NRO accounts with online application; setup takes 7–10 working days. Open one before your visit, or open it on arrival and time the sale accordingly.

Is selling gold as an NRI taxed differently from a resident sale?

The capital gains rate is the same – 12.5% LTCG above 24 months, slab rate STCG below. The administrative differences: NRIs have access to fewer tax-saving exemptions (no Section 54F or 54EC for gold-derived gains in most NRI cases), and repatriation triggers Form 15CA/15CB filings. NRIs also need to be more careful about Indian source documentation because banks scrutinise large NRO-to-foreign transfers more closely than domestic transactions.

Can I get paid in foreign currency for selling gold in India?

No – under FEMA rules, all gold sale transactions in India must be settled in Indian rupees through Indian banking channels. The buyer cannot pay you in USD, GBP, or any other foreign currency. The conversion to your home currency happens only at the repatriation stage from the NRO account, at the bank’s prevailing exchange rate on the day of transfer. This is standard for all NRI-source rupee transactions.

How long does the entire NRI gold sale and repatriation take?

The sale at the branch: 30–60 minutes (XRF, KYC, invoice, IMPS to NRO). NRO credit: same day (within minutes via IMPS or RTGS). Form 15CA filing: same day (online, self-declaration). Form 15CB CA certificate (if needed): 1–3 working days. Bank repatriation processing: 5–7 working days after both forms are submitted. End-to-end: typically 7–10 working days from sale to foreign account credit. Plan your India visit timing accordingly if repatriation must be completed before you leave.

{ “@context”: “https://schema.org”, “@type”: “FAQPage”, “mainEntity”: [ { “@type”: “Question”, “name”: “Can NRIs sell gold in India in Indian rupees?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Yes. Any NRI, OCI cardholder, or PIO can sell gold acquired legally in India, with proceeds settled in Indian rupees to an NRO (Non-Resident Ordinary) account. The price received is identical to what a resident would receive – today’s live IBJA rate × tested purity, with the same XRF testing protocol. The only differences are enhanced KYC (Passport, OCI card, PAN, foreign address proof) and the settlement account being NRO rather than a regular savings account.” } }, { “@type”: “Question”, “name”: “What documents does an NRI need to sell gold in India?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Indian Passport (original), OCI or PIO card (original), PAN card, Aadhaar (if held), Indian address proof, foreign address proof, and NRO account details (number + IFSC). For inherited gold, a Will or family settlement deed is helpful for repatriation. For sales above ₹2 lakh, PAN is mandatory under Rule 114B. For sales above ₹5 lakh, repatriation requires Form 15CB from a CA in addition to the standard Form 15CA self-declaration.” } }, { “@type”: “Question”, “name”: “How does NRI gold repatriation work after the sale?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “After sale proceeds are credited to your NRO account, you can repatriate up to USD 1 million per financial year (April–March) under FEMA rules. The path is: NRO → NRE (rupee-to-rupee, but NRE is freely repatriable) or NRO → foreign account directly. Both require Form 15CA online filing; transactions above ₹5 lakh additionally require Form 15CB CA certificate. Banks typically process the transfer in 5–7 working days once forms are submitted. The USD 1 million limit applies to combined NRI gold repatriation and all other NRO-to-foreign transfers.” } }, { “@type”: “Question”, “name”: “What are the NRI gold tax rules in India?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “NRIs face the same capital gains framework as residents. Gold held over 24 months: long-term capital gains at 12.5% on profit (no indexation, post-July 2024 budget). Gold held under 24 months: short-term gains added to slab income from Indian sources. Cost of acquisition is the original purchase price, or fair market value on the date of inheritance for inherited gold. TDS does not apply to the gold sale itself, but tax must be paid via advance tax or self-assessment before repatriation.” } }, { “@type”: “Question”, “name”: “Do I need an NRO account to sell gold as an NRI?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Not strictly required for the sale itself – small cash sales below ₹1,99,999 can be paid in cash directly. But for any sale above ₹2 lakh (which is most family gold), settlement must move through banking channels, and the natural channel for NRI Indian-source income is an NRO account. If you do not yet have one, almost every Indian bank offers NRO accounts with online application; setup takes 7–10 working days. Open one before your visit, or open it on arrival and time the sale accordingly.” } }, { “@type”: “Question”, “name”: “Is selling gold as NRI taxed differently from resident sale?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “The capital gains rate is the same – 12.5% LTCG above 24 months, slab rate STCG below. The administrative differences: NRIs have access to fewer tax-saving exemptions (no Section 54F or 54EC for gold-derived gains in most NRI cases), and repatriation triggers Form 15CA/15CB filings. NRIs also need to be more careful about Indian source documentation because banks scrutinise large NRO-to-foreign transfers more closely than domestic transactions.” } }, { “@type”: “Question”, “name”: “Can I get paid in foreign currency for selling gold in India?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “No – under FEMA rules, all gold sale transactions in India must be settled in Indian rupees through Indian banking channels. The buyer cannot pay you in USD, GBP, or any other foreign currency. The conversion to your home currency happens only at the repatriation stage from the NRO account, at the bank’s prevailing exchange rate on the day of transfer. This is standard for all NRI-source rupee transactions.” } }, { “@type”: “Question”, “name”: “How long does the entire NRI gold sale and repatriation take?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “The sale at the branch: 30–60 minutes (XRF, KYC, invoice, IMPS to NRO). NRO credit: same day (within minutes via IMPS or RTGS). Form 15CA filing: same day (online, self-declaration). Form 15CB CA certificate (if needed): 1–3 working days. Bank repatriation processing: 5–7 working days after both forms are submitted. End-to-end: typically 7–10 working days from sale to foreign account credit. Plan your India visit timing accordingly if repatriation must be completed before you leave.” } } ] }Visiting India and planning to sell inherited gold?

Visit your nearest Attica Gold branch – XRF testing, NRI-specific KYC, IMPS to your NRO account.

Get Instant Valuation

Free evaluation · No obligation · Instant offer

🔒 Your details are safe and confidential