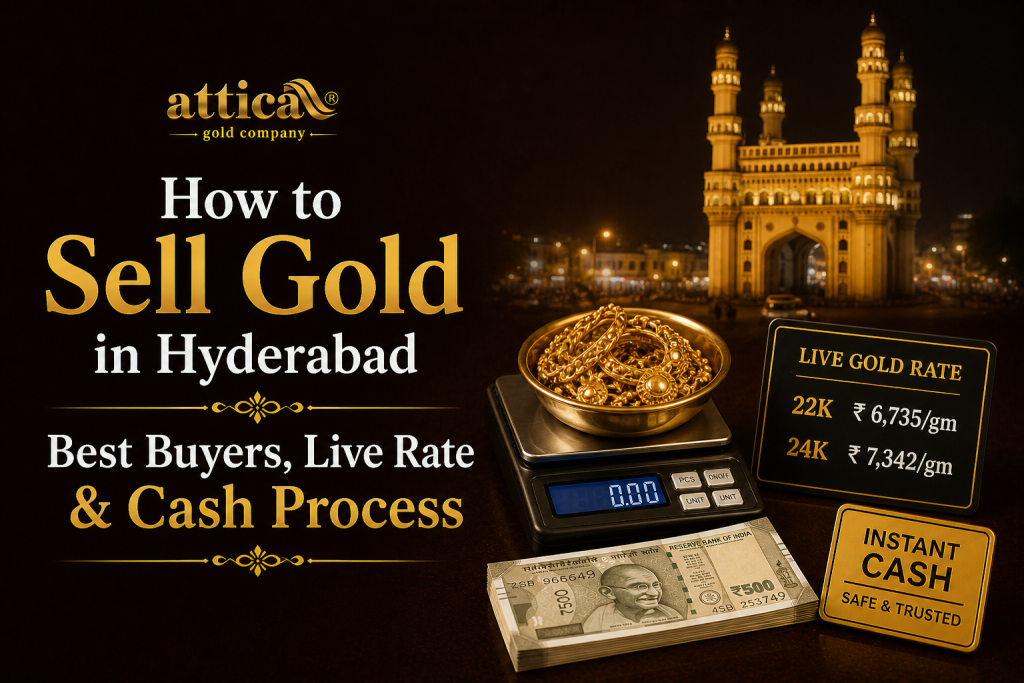

⚡ Quick Answer

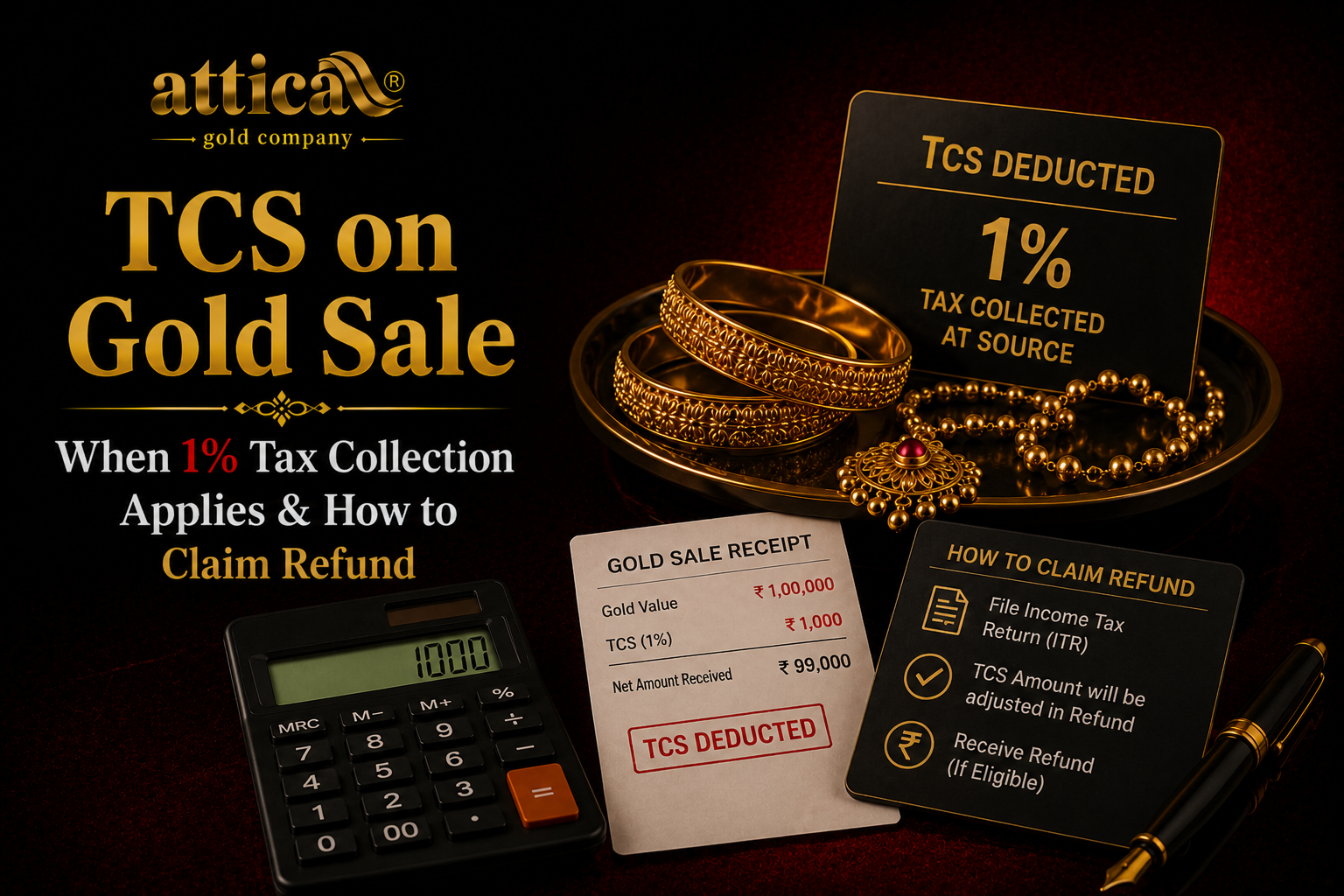

TCS on gold purchase (Tax Collected at Source) at 1% applies when a buyer pays cash above ₹2 lakh for jewellery – the seller (jeweller/buyer) collects 1% of the transaction value and deposits it against the purchaser’s PAN. For gold sale (you selling old gold), TCS on gold sale applies in specific cases – most retail gold-selling transactions are NOT subject to TCS at the seller’s hand, but TDS (Tax Deducted at Source) may apply at higher thresholds. TCS deposited shows up in your Form 26AS; how to claim TCS refund: file ITR, claim the TCS as a tax credit against your total tax liability – any excess is refunded. Always consult a CA for specifics. This is general information, not tax advice.

📌 Key Facts At A Glance

- TCS on gold purchase: 1% on cash transactions exceeding ₹2 lakh – collected by jeweller from buyer.

- TCS on gold sale (when you sell old gold): generally not applicable at retail-buyer level; TDS rules differ.

- Tax on gold in india covers: GST on jewellery (3%), capital gains tax on gold (12.5% LTCG / slab STCG), and TCS/TDS where applicable.

- TCS deposited shows in Form 26AS under PAN – verify before filing ITR.

- How to claim TCS refund: report TCS in ‘Schedule TCS’ of ITR; net of total tax liability is refunded.

- TDS on gold sale: not commonly applied; specific high-value or trade scenarios may attract Section 194-O / 194-Q.

- RBI rule: cash transactions above ₹2 lakh are restricted under Section 269ST of the Income Tax Act – bank transfer is mandatory.

Understanding Tax on Gold in India Beyond Capital Gains

Most retail sellers know about capital gains tax on gold – the tax on the profit when you sell your gold. But gold tax in india has multiple layers, and one that often surprises people is TCS (Tax Collected at Source). TCS isn’t a tax in the conventional sense – it’s a collection mechanism the government uses to track high-value transactions. The buyer (or seller, depending on the section) collects a small percentage at the time of transaction and deposits it against your PAN. You then claim it back as a tax credit when filing your ITR.

This guide explains: when TCS on gold sale or TCS on gold purchase applies, the ₹2 lakh threshold and 1% rate, how to find TCS in your Form 26AS, how to claim TCS refund through ITR, and what TDS on gold sale rules might also apply. As always, this is general information; specific high-value or unusual situations should be reviewed with a Chartered Accountant.

TCS on Gold Purchase – When You’re Buying

Section 206C(1F) of the Income Tax Act requires sellers (jewellers, bullion dealers) to collect TCS at 1% on cash transactions for jewellery exceeding ₹5 lakh and for bullion exceeding ₹2 lakh in value. This applies when YOU are the buyer. The jeweller adds 1% to the bill, deposits it against your PAN, and reflects it in your Form 26AS. You can claim this back in your ITR.

Note: cash payments above ₹2 lakh are separately restricted under Section 269ST regardless of TCS. Bank transfer (NEFT/RTGS/UPI) is the practical norm for any large transaction.

- Also Read: Live Gold Price Today

TCS on Gold Sale – When You’re Selling

TCS on gold sale (i.e., when you’re the seller of old gold) is structured differently. The 1% TCS provisions of Section 206C(1F) primarily target cash purchases above the threshold by buyers. When you sell your old gold to a buyer like Attica Gold, the buyer pays you the net amount (after deductions); TCS may or may not apply depending on transaction structure:

| Scenario | TCS / TDS implication | Practical effect |

| Retail sale by individual to chain buyer (any amount) | Generally no TCS at sale | Buyer pays you full net; you handle CG tax in ITR |

| Sale by individual to refinery, lot >₹50 lakh | TDS u/s 194Q may apply (0.1%) | Refinery deducts; goes to your 26AS |

| Sale by trader / business to buyer | Both TDS and GST may apply | Trader’s GST registration and tax compliance differ |

| Sale via online aggregator (e-commerce) | TCS u/s 194-O at 1% | Aggregator collects 1%; reflects in 26AS |

For the typical individual selling 50–500g of family gold to a brick-and-mortar buyer like Attica, TCS at the sale step is uncommon. The applicable tax is the capital gains tax on gold computed in your ITR.

How to Verify TCS in Your Form 26AS

- Login to incometax.gov.in with your PAN.

- Navigate to ‘My Account’ → ‘View Form 26AS’ (it redirects to TRACES portal).

- Verify your DOB, accept the disclaimer, and download Form 26AS as PDF or HTML for the relevant assessment year.

- Look under ‘Part C’ (TDS) and ‘Part D’ (TCS) sections. Any TCS collected against your PAN – by jewellers, e-commerce aggregators, refineries, etc. – appears here with the date, deductor’s TAN, and amount.

- Cross-check with your purchase or sale documentation: the seller/deductor should have given you a TCS certificate (Form 27D); confirm the entries match.

- If TCS appears in 26AS but you don’t recognise it, contact the deductor (their TAN is in 26AS); discrepancies need correction before ITR filing.

How to Claim TCS Refund in Your ITR

- After computing your total tax liability (capital gains, salary, other income), check the TCS amount from Form 26AS.

- In your ITR (typically ITR-2 or ITR-3 if you have capital gains), navigate to ‘Schedule TCS’ (Tax Collected at Source).

- Enter the deductor’s TAN, transaction date, gross amount, and TCS amount as shown in 26AS.

- The TCS automatically reduces your total tax liability. If the TCS exceeds your total tax payable, the difference is refunded to your bank account.

- Verify the ITR via Aadhaar OTP, EVC, or signed ITR-V. The refund is processed by the IT Department within 30–90 days of e-verification.

- Track refund status under ‘Refund/Demand Status’ on the e-filing portal. Refunds are credited to the bank account pre-validated against your PAN.

Common TCS Confusion: Gold Loan vs Gold Sale

A frequent misconception: people think TCS applies when they take a gold loan. It does not – a gold loan is a secured borrowing, not a purchase or sale. No TCS on gold purchase or TCS on gold sale applies to gold loans. The bank/NBFC charges interest, processing fees, and (sometimes) GST on the service component, but no TCS.

Where TCS does intersect with gold loans: if you default on a gold loan and the bank auctions your pledged gold, the auction proceeds may attract TCS at the buyer end (since it’s now a fresh purchase). The borrower (you) is no longer involved in that step.

💰 Get the Best Price for Your Gold Today

Instant valuation • Transparent pricing • 100% secure & trusted

TDS on Gold Sale: Rare but Real Cases

TDS (Tax Deducted at Source) on gold sale is much less common than TCS but applies in specific scenarios:

- Section 194-O: e-commerce gold aggregators collect 1% TDS on sales facilitated through their platform – applies if you sell gold via an online aggregator.

- Section 194-Q: a buyer purchasing goods from a single seller exceeding ₹50 lakh in a financial year deducts 0.1% TDS – applies for very large gold trades, mostly business-to-business, rarely retail.

- Section 195: TDS on payment to non-residents – applies if you (an NRI) sell gold in India and receive payment; the buyer must deduct TDS at applicable rates.

For most resident retail sellers selling family gold to a chain buyer, none of these TDS sections will apply. Your only direct tax obligation is the capital gains tax computed in your ITR.

Worked Example: TCS Refund Scenario

Suppose you bought 100g of gold jewellery in March 2025 from a retail jeweller for ₹7 lakh, paid in cash (uncommon but illustrative). The jeweller collected 1% TCS = ₹7,000 against your PAN. Your Form 26AS for FY 2024-25 shows ₹7,000 under Part D (TCS).

When filing ITR for FY 2024-25: your total tax liability (salary + any other income) is, say, ₹1,80,000. Your TDS from salary already deducted: ₹1,50,000. Adding the TCS from gold purchase: ₹1,50,000 + ₹7,000 = ₹1,57,000 already credited. Net tax payable: ₹1,80,000 − ₹1,57,000 = ₹23,000 (you pay this via Self-Assessment Tax).

If, hypothetically, your total tax was only ₹1,55,000 and TDS+TCS was ₹1,57,000, you’d get a refund of ₹2,000. Either way, the TCS from gold purchase is fully credited – you never lose it; how to claim TCS refund is just standard ITR filing with Schedule TCS.

Key Documents to Keep for TCS Claims

- Form 27D – TCS certificate issued by the deductor (the jeweller/buyer who collected TCS). It’s their statutory obligation.

- Form 26AS – your tax credit statement; TCS shows under Part D.

- Original purchase or sale invoice – must match the TCS amount and date.

- Bank statement showing the cash/transfer that triggered the TCS – provides corroboration.

- Final ITR-V acknowledgement – proof that you claimed the TCS in your return.

Why Choose Attica Gold for Sale With Clean Documentation – Your Wait Is Over

TCS on gold sale and TCS on gold purchase are mechanisms to track high-value transactions, not additional taxes. If TCS is collected, it’s fully creditable against your tax liability – you never lose the money, you just claim it back through ITR. The administrative trick is to keep clean documentation: Form 27D from the deductor, matching invoices, and a verified Form 26AS at year-end.

Attica Gold’s process is built for this clean documentation: every sale generates a printed GSTIN-stamped invoice with weight, purity, IBJA-linked rate, deductions, net amount, and (if applicable) any TDS/TCS reference. ISO 9001:2015 certified, ~200+ branches across South India, NEFT/RTGS payment within 24 hours, full digital and physical receipts. Whether the sale triggers TCS or not, you get the paperwork to file ITR cleanly. Tax on gold in india is manageable when the sale-side documentation is right. Your wait is over.

Frequently Asked Questions

When does TCS on gold purchase apply?

Under Section 206C(1F), TCS at 1% applies when a buyer pays cash exceeding ₹2 lakh (for bullion) or ₹5 lakh (for jewellery). Note that cash transactions above ₹2 lakh are also restricted under Section 269ST. In practice, large gold purchases happen via bank transfer and TCS may apply based on transaction structure. Verify with the seller and your CA.

Does TCS on gold sale apply when I sell old gold to a buyer?

For typical individual sellers selling old jewellery to a brick-and-mortar buyer, TCS at the sale step generally does not apply. The applicable tax is capital gains tax computed in your ITR. TCS may apply in specific scenarios – sale via online aggregator (Section 194-O), trade transactions over ₹50 lakh (Section 194-Q), or NRI sales (Section 195).

How do I check if TCS was collected on my gold transaction?

Login to incometax.gov.in, view Form 26AS (redirects to TRACES portal). Under Part D (TCS), you’ll see all TCS collected against your PAN, with dates, deductor TANs, and amounts. The deductor must also issue you Form 27D as a TCS certificate.

How to claim TCS refund in my ITR?

In your ITR, fill Schedule TCS with the TCS details from Form 26AS – deductor TAN, date, gross amount, TCS amount. The TCS reduces your total tax liability automatically. If TCS exceeds your tax payable, the excess is refunded to your pre-validated bank account within 30–90 days of e-verification.

Is TDS on gold sale common in retail transactions?

No – TDS on gold sale typically applies only to e-commerce sales (Section 194-O), large B2B transactions over ₹50 lakh (Section 194-Q), or sales by non-residents (Section 195). Most retail individual sellers selling family gold to a chain buyer like Attica face no TDS at the sale step.

I’m an NRI selling gold in India – does TDS apply?

Yes – under Section 195, the buyer must deduct TDS on payments to non-residents at applicable rates (typically 20% or as per DTAA between India and the NRI’s country of residence). The TDS amount is reflected in your Indian Form 26AS; you claim it as credit when filing ITR in India and (where applicable) in your country of residence.

Can I avoid TCS by paying gold purchase via UPI instead of cash?

Cash-payment thresholds (Section 269ST) are about cash specifically; UPI/NEFT/RTGS are exempt from those cash limits. However, Section 206C(1F) TCS at 1% is triggered by transaction value above the threshold regardless of payment mode. UPI doesn’t bypass TCS for high-value purchases – it just removes the cash-payment restriction. Always verify with the seller and your CA.

Sources & References

This page references and is informed by the following authoritative sources. Last verified: May 2026.

[1] Section 206C – Tax Collection at Source on Sale of Specified Goods – Income Tax Department, Government of India. https://www.incometax.gov.in/

[2] Section 269ST – Cash Transaction Limits – Central Board of Direct Taxes (CBDT). https://incometaxindia.gov.in/

[3] Form 26AS Access via TRACES Portal – Tax Reconciliation, Analysis and Correction Enabling System. https://www.tdscpc.gov.in/

[4] Section 194-Q & Section 194-O – TDS Provisions – Income Tax Department, Government of India. https://www.incometax.gov.in/

[5] Section 195 – TDS on Payments to Non-Residents – Income Tax Department, Government of India. https://www.incometax.gov.in/

{ “@context”: “https://schema.org”, “@type”: “FAQPage”, “mainEntity”: [ { “@type”: “Question”, “name”: “When does TCS on gold purchase apply?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Under Section 206C(1F), TCS at 1% applies when a buyer pays cash exceeding ₹2 lakh (for bullion) or ₹5 lakh (for jewellery). Note that cash transactions above ₹2 lakh are also restricted under Section 269ST. In practice, large gold purchases happen via bank transfer and TCS may apply based on transaction structure. Verify with the seller and your CA.” } }, { “@type”: “Question”, “name”: “Does TCS on gold sale apply when I sell old gold to a buyer?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “For typical individual sellers selling old jewellery to a brick-and-mortar buyer, TCS at the sale step generally does not apply. The applicable tax is capital gains tax computed in your ITR. TCS may apply in specific scenarios – sale via online aggregator (Section 194-O), trade transactions over ₹50 lakh (Section 194-Q), or NRI sales (Section 195).” } }, { “@type”: “Question”, “name”: “How do I check if TCS was collected on my gold transaction?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Login to incometax.gov.in, view Form 26AS (redirects to TRACES portal). Under Part D (TCS), you’ll see all TCS collected against your PAN, with dates, deductor TANs, and amounts. The deductor must also issue you Form 27D as a TCS certificate.” } }, { “@type”: “Question”, “name”: “How to claim TCS refund in my ITR?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “In your ITR, fill Schedule TCS with the TCS details from Form 26AS – deductor TAN, date, gross amount, TCS amount. The TCS reduces your total tax liability automatically. If TCS exceeds your tax payable, the excess is refunded to your pre-validated bank account within 30–90 days of e-verification.” } }, { “@type”: “Question”, “name”: “Is TDS on gold sale common in retail transactions?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “No – TDS on gold sale typically applies only to e-commerce sales (Section 194-O), large B2B transactions over ₹50 lakh (Section 194-Q), or sales by non-residents (Section 195). Most retail individual sellers selling family gold to a chain buyer like Attica face no TDS at the sale step.” } }, { “@type”: “Question”, “name”: “I’m an NRI selling gold in India – does TDS apply?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Yes – under Section 195, the buyer must deduct TDS on payments to non-residents at applicable rates (typically 20% or as per DTAA between India and the NRI’s country of residence). The TDS amount is reflected in your Indian Form 26AS; you claim it as credit when filing ITR in India and (where applicable) in your country of residence.” } }, { “@type”: “Question”, “name”: “Can I avoid TCS by paying gold purchase via UPI instead of cash?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Cash-payment thresholds (Section 269ST) are about cash specifically; UPI/NEFT/RTGS are exempt from those cash limits. However, Section 206C(1F) TCS at 1% is triggered by transaction value above the threshold regardless of payment mode. UPI doesn’t bypass TCS for high-value purchases – it just removes the cash-payment restriction. Always verify with the seller and your CA.” } } ] }Need clean documentation for your gold sale?

Attica Gold issues GSTIN-stamped invoices with all line items required for ITR filing and TCS/TDS reconciliation.

Get Instant Valuation

Free evaluation · No obligation · Instant offer

🔒 Your details are safe and confidential